What is DeFi? The Ultimate Guide to Decentralized Finance in 2025

Published on: 28 Nov 2025

Imagine a financial system that never sleeps. It doesn’t close on weekends, it doesn’t care about your credit score, and it doesn’t require a photo ID to open an account. It is open to anyone with an internet connection, anywhere on the planet.

Learn more about our Website services

This isn’t a utopian dream. It is happening right now, managing hundreds of billions of dollars in assets. It is called DeFi, or Decentralized Finance.

If cryptocurrency is digital money, DeFi is the digital banking system built on top of it—but with one crucial difference: there are no banks.

In this ultimate guide, we are going to dismantle traditional finance and rebuild it block by block to show you how DeFi is reshaping the global economy in 2025 and beyond. Whether you are looking to earn passive income that puts high-street savings accounts to shame, or you simply want true ownership of your assets, this is your starting line.

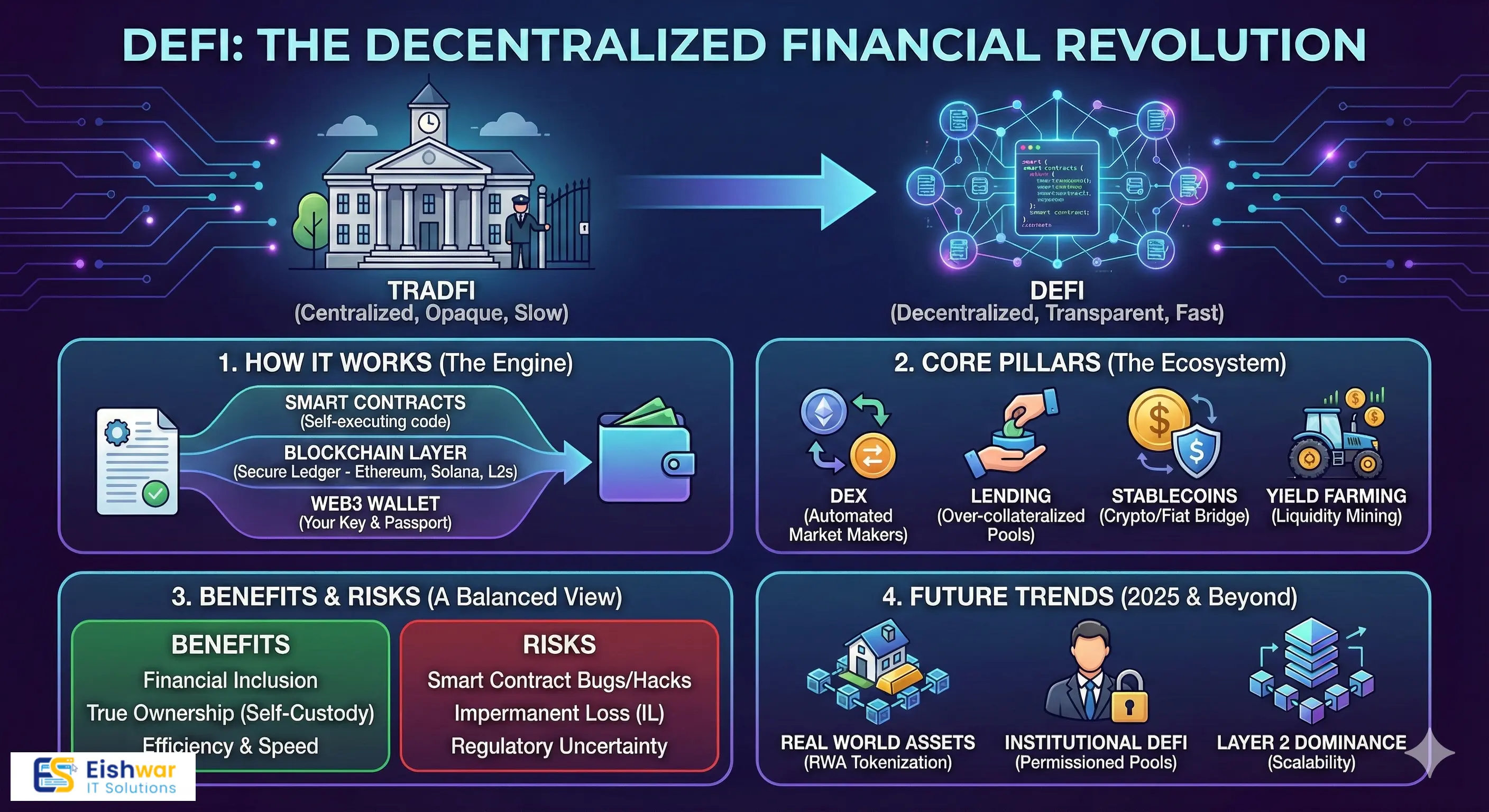

1. What is DeFi Actually?

At its simplest, DeFi (Decentralized Finance) is an umbrella term for financial services built on public blockchains, primarily Ethereum.

In the traditional financial world (often called "TradFi"), central intermediaries control everything. Banks, brokerages, and exchanges act as gatekeepers. They hold your money, they approve your loans, and they facilitate your trades—taking a cut at every step and introducing a single point of failure.

DeFi removes the middleman. It replaces the banker with code.

The "Money LEGOs" Concept

Think of DeFi protocols as open-source "money LEGOs." Because they are built on public blockchains, different decentralized applications (dApps) can interact with each other permissionlessly.

You can take a stablecoin from Protocol A, lend it on Protocol B to earn interest, and use the interest-bearing receipt as collateral to trade on Protocol C. This "composability" allows for complex financial strategies that are impossible in the siloed world of traditional banking.

TradFi vs. DeFi: A Quick Comparison

| Feature | Traditional Finance (TradFi) | Decentralized Finance (DeFi) |

|---|---|---|

| Controller | Banks, Governments, Central Banks | Code and Communities (DAOs) |

| Access | Permissioned (KYC, Credit Checks) | Permissionless (Anyone with a wallet) |

| Transparency | Opaque (Hidden books) | Transparent (Public ledger) |

| Speed | Slow (Days for settlement) | Fast (Minutes or seconds) |

| Custody | The Bank holds your money | You hold your money (Self-custody) |

| Markets | Closed weekends/holidays | 24/7/365 |

2. The Engine Room: How DeFi Works

If there are no banks, who runs the show? The magic of DeFi relies on three core technologies.

A. Smart Contracts: The Invisible Banker

A smart contract is a self-executing program stored on a blockchain that runs when predetermined conditions are met.

Think of a vending machine. You don't need a cashier. You put in money ($2), select an item (Soda), and the machine automatically releases the product.

In DeFi, a smart contract might say: "If User A deposits 1 ETH as collateral, allow them to borrow 1,500 USDC. If the value of their 1 ETH collateral drops below $1,600, automatically sell it to repay the loan."

This happens instantly, without human intervention or bias.

B. The Blockchain Layer

Smart contracts need a secure foundation to live on. While Ethereum is the original home of DeFi, the ecosystem in 2025 is multi-chain. High-speed networks like Solana, and Layer-2 scaling solutions for Ethereum like Arbitrum and Optimism, are now major hubs for DeFi activity, offering faster and cheaper transactions.

👉 Don't wait for the perfect moment; turn your vision into reality today.

Free ConsultationC. The Web3 Wallet: Your Passport

To interact with DeFi, you don't create an account with an email and password. You connect a non-custodial crypto wallet (like MetaMask, Phantom, or Rabin). This wallet holds your private keys and acts as your universal login across the entire decentralized web.

3. The Core Pillars of the DeFi Ecosystem

The DeFi ecosystem has replicated almost every service offered by traditional wall street, often with greater efficiency. Here are the main categories.

A. Decentralized Exchanges (DEXs)

Examples: Uniswap, Curve, Jupiter.

A Centralized Exchange (CEX) like Coinbase uses an "order book" to match buyers and sellers, much like the New York Stock Exchange.

A DEX allows you to swap tokens peer-to-peer without giving up custody of your assets. They don't use order books. Instead, they use Automated Market Makers (AMMs).

- How AMMs Work: Imagine a big bucket containing two types of tokens (e.g., ETH and USDC). This is a Liquidity Pool. When you want to trade ETH for USDC, you put ETH into the bucket and take USDC out. The price is determined mathematically by the ratio of the two assets in the bucket.

B. Lending and Borrowing Markets

Examples: Aave, Compound.

In TradFi, you put money in a savings account, the bank pays you 0.5% interest, lends your money out at 6%, and keeps the profit.

In DeFi, you lend your crypto directly to the protocol’s "pool" and borrow against it.

- Lenders: Deposit crypto to earn interest (yield), paid by borrowers.

- Borrowers: Deposit crypto as collateral to borrow other assets instantly.

Crucial Note: DeFi borrowing is almost always over-collateralized. Because there are no credit checks, you must deposit more value than you borrow. If you want to borrow $100 worth of USDC, you might need to deposit $150 worth of ETH. This protects the lender if the borrower defaults.

C. Stablecoins: The Bridge

Examples: USDC (Fiat-backed), DAI (Crypto-backed decentralized).

Cryptocurrency is volatile. You can't easily use Bitcoin for rent if its value drops 10% overnight. Stablecoins are tokens pegged to a stable asset, usually the US Dollar. They are the lifeblood of DeFi, allowing users to lock in profits or transact without volatility while remaining on-chain.

D. Yield Farming and Liquidity Mining

This is the "turbo-charged" aspect of DeFi that attracts many investors seeking high returns.

When you provide funds to a DEX's liquidity pool (making trading possible for others), you earn a cut of the trading fees. This is basic yield.

Yield Farming involves moving your assets around different DeFi protocols to maximize returns. Often, protocols will incentivize you to use their platform by paying you bonus rewards in their own "governance token" on top of the standard fees. This is called Liquidity Mining.

Warning: While yields can sometimes hit double or triple digits, these strategies carry significant risks, including impermanent loss and smart contract bugs.

4. The Massive Benefits of Decentralization

👉 Free Website Audit

Get Free AuditWhy bother moving away from traditional banks?

1. Financial Inclusion

There are roughly 1.4 billion unbanked adults globally. They lack access to savings, credit, or safe ways to transfer money. DeFi requires only a smartphone and internet access to plug them into the global financial grid.

2. True Ownership (Self-Custody)

When your money is in a bank, it is technically the bank's liability to you. In times of crisis, banks can freeze accounts or limit withdrawals. In DeFi, you hold the private keys. Nobody can confiscate your assets if you secure your wallet properly.

3. Transparency and Composability

Every transaction and smart contract is visible on the blockchain. You don't have to trust that a protocol is solvent; you can verify it on-chain in real-time.

4. Efficiency and Speed

Moving $10 million internationally via swift can take days and cost a fortune in fees. In DeFi, it can be done in seconds for a fraction of the cost, regardless of borders.

5. The Dark Side: Major Risks in DeFi

DeFi is often called the "Wild West" of finance. While it has matured significantly by 2025, the risks are very real. This is not a risk-free savings account.

A. Smart Contract Risk (Bugs and Hacks)

If the code that runs the protocol has a flaw, hackers can exploit it and drain the funds. While top-tier protocols undergo rigorous audits, hacks still happen.

Rule: Never put more money into a single protocol than you are willing to lose.

B. Impermanent Loss (IL)

This is a complex risk specific to providing liquidity on DEXs like Uniswap. If the price of the two tokens you deposited changes drastically relative to each other after you deposit them, when you withdraw, you might end up with less dollar value than if you had just held the tokens in your wallet. The loss is "impermanent" because it only becomes realized when you withdraw, but it is a very real danger.

C. Regulatory Uncertainty

Governments are still figuring out how to regulate DeFi. In 2025, frameworks like MiCA in Europe have provided some clarity, but in other regions, regulators may crack down on interfaces that allow access to certain protocols, creating uncertainty for users.

D. User Error and Scams

There is no "forgot password" button in DeFi. If you lose your private key, your funds are gone forever. Furthermore, phishing scams designed to trick you into signing malicious transactions are rampant.

6. The Future of DeFi: 2025 and Beyond

DeFi is no longer just about trading meme coins. It is maturing and integrating with the real economy.

The Rise of Real World Assets (RWA)

This is the biggest trend of the mid-2020s. Protocols are bringing off-chain assets—like US Treasury Bills, real estate, corporate credit, and gold—onto the blockchain via tokenization.

- Why it matters: It allows DeFi users to earn sustainable yields backed by real-world revenue streams, rather than just relying on crypto market volatility. It bridges the multi-trillion-dollar traditional finance world with the efficiency of blockchain.

Institutional DeFi

Major financial players are no longer ignoring DeFi; they are building "walled gardens." We are seeing "permissioned DeFi" pools where participants must pass KYC (Know Your Customer) checks to comply with regulations, allowing institutions to access DeFi yields safely.

👉 Free Homepage Demo

Book DemoLayer 2 Dominance

Ethereum mainnet is now primarily a settlement layer for large players. Everyday DeFi users operate on Layer 2 solutions (like Arbitrum, Base, and Optimism) which offer the security of Ethereum but with transaction fees measured in cents rather than dollars.

Conclusion: Taking the Red Pill

DeFi is a paradigm shift. It is a movement away from "trusting" institutions with our financial livelihood toward "verifying" everything through code.

It offers unparalleled opportunities for yield generation, access to capital, and financial sovereignty. However, it demands a higher level of personal responsibility than the traditional system.